Digital Protectors of the New Era: Cyber Insurance by Onur Korucu

Demystifying Cyber Insurance

Hello everyone! I'm delighted to have this opportunity to talk about a topic that has been making waves in recent years – Cyber Insurance. My voice is a bit scratchy due to cold, but I hope the content we have prepared for you today will be enlightening. I am Honor Corio, a senior data protection, GRC, and cybersecurity manager at A UK and Ireland. My past roles included positions in KPMG, PWC, and Grant Thorton where I assisted businesses in creating robust, tailor-made cybersecurity governance structures that mitigate risk.

About Cyber Insurance

Cyber insurance, also known as cyber risk insurance or cyber liability insurance, is a coverage designed to protect businesses from threats in the digital age, such as data breaches or malicious hacks on their computer systems. Its primary purpose is not to improve cybersecurity but to transfer residual risk. It is a valuable tool, helping organisations mitigate the financial impact of cyber-related incidents and providing much-needed post-incident services such as forensics, incident response, legal aid, and PR advice.

Understanding Cyber Risks

Our increasing reliance on networks and the internet has amplified cyber risks, particularly during the pandemic. Cyber risks result from the use (and misuse) of information and communication technologies, compromising confidentiality, availability, and integrity of data or services. These risks can cause business disruptions, infrastructure breakdowns, and even physical damage, making cyber insurance a necessity for individuals and organisations alike.

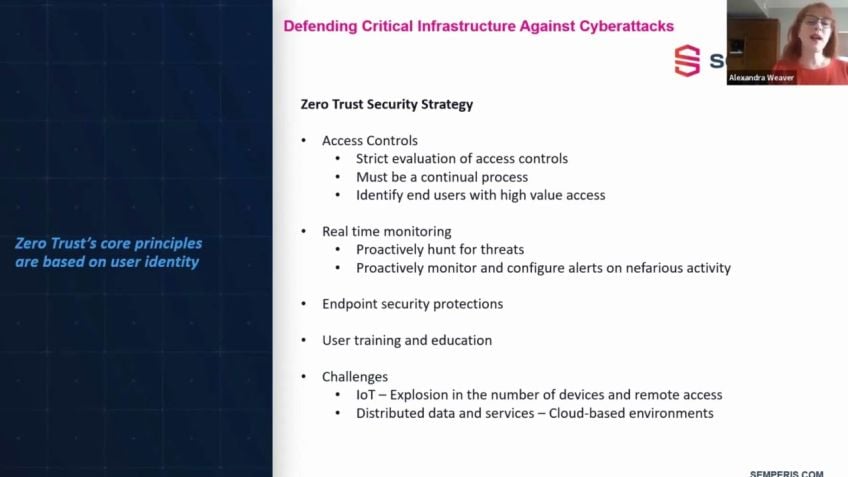

Here are some categories of cyber risks:

- Physical Damage: Cyberattacks can cause physical harm to assets. An example could be a hacker triggering fire sprinklers remotely that can lead to tangible damage.

- Business Interruption: Cyberattacks might halt business operations affecting revenue and reputation.

- Reputational Damage: Breaches can tarnish a business's reputation, leading to financial repercussions and loss of customer trust.

- Privacy Claims: Data breaches leading to exposure of sensitive customer data can result in costly lawsuits.

The Relationship between Cyber Insurance and GDPR

Cyber insurance is closely allied with GDPR. An insurance policy might cover data breach associated fines and penalties,provided they are deemed insurable by a GDPR regulator. This underlines the importance of planning ahead from a financial standpoint to face possible compliance penalties.

Personal Cyber Insurance

As technology permeates into our personal lives, the need for personal cyber insurance rises steadily. This covers protection against identity theft, data loss recovery, cyberbullying, network extortion, fraudulent transactions, and more. It's important to remember that while providing many benefits, digitization opens the door to several risks too.

Challenges in Cyber Insurance

Despite its potential, cyber insurance still grapples with several challenges such as negative behaviors incentivized by coverage and misunderstanding of the coverage's purpose. However, these issues can be addressed with comprehensive risk assessment and mitigation strategies.

Final Thoughts

As we delve further into the digital era, I believe cyber insurance will become even more crucial. We might see the emergence of newer forms of insurance such as cloud computing insurance, IOT insurance, AI insurance, and Blockchain insurance. With its potential to improve cybersecurity practices, cyber insurance will undoubtedly become instrumental in managing everyday risk.

Thank you once again for your time and participation. As we navigate this digital world, I look forward to your valued contributions in the field of cyber insurance. Wishing you the very best for this journey!

Video Transcription

Hello, everybody. Before I start, I want to say very sincere hi to everyone and thank you all for taking time and attend this session today. I'm very proud to show the woman power together once again and with participation from many different locations in the world.And it's a great to be part of woman intact family. I would like to express my gratitude once again to giving the chance to meet you. I hope you don't mind my voice because my voice is a little bit scratchy due to cold. I have. Anyway, I hope the content we are prepared for. You will be useful. First of all, uh I want to introduce myself to you. My name is Honor Corio and I am working as a senior data protection, GRC and cybersecurity manager at A UK. And Ireland. Previously, I worked in multinational professional services companies such as KPMG PWC and Grant Thorton. And I help organizations create uh robust tailor made and well established information and cybersecurity governance structures and data protection practices that mitigate the risks they face in their business, in their sectors and help them to comply with regulatory requirements like GDPR computation issues.

And my current role is in a technology company and we are empowering companies in areas such as GRC cybersecurity data protection. By using different technology solutions. It can be Microsoft and it can be other, you know, useful technology solutions. Along my side, I continue to be a woman in technology representative in large scale international communities like AAA Europe, AAA Asia IAPP by having a presence in conference and seminars. And I published my first book last year, it was about a correlation risk management and GDPR and the cybersecurity. And so today, I'm going to talk about very trending topics of recent years. This is Cyber insurance and in the section, we will focus on the definition of cyber insurance and the benefits of cyber insurance. And I think the importance because I think people cannot understand the mo this is very important thing for our future. So maybe I can start like that. My first encounter with the concept of cyber insurance dates back to 78 years ago. And I am very happy witness the studies and investments made in this field because we were working on this cyber insurance issues together with Microsoft right now.

And I'm really happy uh because we can use, we can understand the importance of cyber insurance. If we can continue with our slides, let's start with cyber risk because cyber risk which are the root cause of cyber insurance have increased drastically during the pandemic. And so and risk emerging for use of information and communication technology that compromises, you know, we've got a triology, this confidentiality, availability and integrity of the data or services. The empowerment of operational technology eventually leads to business disruption, infrastructure breakdown and physical damage to humans and properties.

Some risk either cause naturally or it can be manmade where the latter can emerge for human failure or cyber criminality. Cyber war and cyberterrorism. It is very, very, you know uh familiar right now, everybody used to it because this cyber blink, you are using very clever phone machine cars, everything um can cause cyber risks right now. So it is characterized by in interdependencies, professional extreme events, high uncertainty with respect to data and modeling approach and risk of change. And in a uni of cyber risk is risk of change because you know, time is changing after pandemic, new technologies and regulations continues to affect the nature of cyber risk. For example, further technological innovations such as internet of things, Iot artificial intelligence, healthtech robotics, think about five G Blockchain will further increase cyber risks and li emerging of new and unforeseen risks. And the changing risk comes. Um the need for better insurance and the development of connected technologies or cyberspace is leading to business opportunities as well as increasing risks. This provides space to develop new and improve existing insurance leading to premium products and two size. These opportunities today feel uh full potential.

Non conventional approach is needed. While in insurance markets, uh needs require uh to build a providing stability by being stable. When it comes to cyber risk market, it needs to require development change in risks as well as markets will happen ever more quickly. So uh in the not too distant feature, only the insurance who know how to service their customer with these changes will remain and understanding cyber risk. This is a fundamental role for the future of the insurance is it's a good start for them. And if you look at the slide afterwards, we understand what a cyber is. We can talk about what is cyber loss because we generally always think about if you will lose something by cyberspace, it can be very digital, but cyber loss is not just the who digital risk, it splits over the physical world, tangible assets as well. For example, hacking into fire protection sprinkler system cloud leads to clothing and damage the physical property, an integrated swe of Cyprus uh critical to fully intangible assets which leaves organization exposed to a much wider scale of damage. Because cyber insurance has historically been focused on digital assets such as clients, personal data. Uh the transactional data tangible assets are generally not being insured. The increase in cyberattacks along with its wider impact has lead clients and insurance to take.

And this ring issues and Macon effect on the insurance lines like personal reputation, physical dam damage and intellectual properties in general. Uh cyber risk can be categorized according to several um dimensions. If you look at it here, you can understand it's not just about physical damage or just business interruption. It's of course and uh related to reputational damage and privacy claims and fishing because in pandemic you experience a lot of ransom mayors and for example, the float earthquake or fire like can cause this physical damage too. So you can think about, there are a lot of different examples. Also its digital assets like data, it extends far deeper across other lines of risk. The bulk of damage, cyber events may actually be physical assets, especially if cybersecurity is being used to gain access at physical assets.

For example, your home, you've got a hacking and you can be hacked because you a lot of power and you got an alarm system to gain entry and steal possessions. And for example, your property like hacking control systems for malicious purposes including sabotage, changing temperatures in comput warehouse to destroy stock setting of fire sprinkler systems to uh evacuate building. And for example, you're not driving Tesla or very electronic cars.

And so your vehicle theft by controlling on board computer team, I immobile cars and aviation shipping, stealing customers, personal information to onboard internet access. And it's very typical personal data breach scenario in this, you know era. And for this reason, cyber risk mm is being recognized as an operational risk and monitor separately from general operational risks So we have to, we have to understand it's not just about our physical issues or just business interruptions. It's really about your personal life daily routine and it's really impacted everywhere. And then the question is then what is the cyber insurance? The cyber insurance? We can refer that cyber risk insurance or cyber loyalty insurance too is a form of coverage designed to protect your business from threats in digital age such as data breach, malicious cyber hacks on their computer systems. And it is very important to remember that the primary purpose of cyber insurance is not improve cybersecurity but to transfer your residual risk. It's not a silver bullet for cybersecurity challenge, but this is very important. It's not just a product to just focused on post incident. Did this?

Cyber insurance included forensic analysis, incident response, legal services and peer advice. So with this way, by which cyber insurance has some positive effects, cyber security and risk management can be identified. I mean that it's like assessing your risk profile and secure the practices or if you have a company, you can understand your posture, your maturity of cyber security and then linking these risk profiles with best practices and the financial incentives and then raising awareness of risk and providing access for the services to access your client's profile.

They can identify potential risks, poor cyber hygiene and bad practices via intentional risk management. Implement new controls and previously identify vulnerabilities. I think it's like a complex work because in professional services, we always started with risk management and understand our clients needs and the maturities for the cybersecurity information security and data protection area. And with the cyber insurance, you can agree that business became dependent on computer networks and the internet because you can profile your clients, you can profile your companies or you can profile your own internet, your own digital era risks. I'm in that and Cyber insurance has two primary purposes. This depending on the needs per child, per per purchase purchase. Cyber insurance provides a risk transfer mechanism. This enables an organization to spread and differ um financial uh risk to uh another party to cover at least of costuming from a cyber incident if used properly. This financial backstop serves as the last step in the risk management process. It emphasis that Cyber insurance is intended to transfer residual risk to risk that in other uh cyber risk management practices not mitigate and who needs this cyber insurance.

This is very important area because any business which had an online component or one that sends or store electronic data might benefit from Cyber insurance. As may an organization that relies on technology to conduct its operations, which is pretty much every business in this world.

And if we can continue in here, you can understand that this Cyber insurance is very, very familiar with uh GDPR because while many insurance policies provide comprehensive coverage for fines, penalties associated with the data breach. A GDPR regulator will be the one of the determine whether fines are insurable or not based on GDPR insurance requirements. This could mean business owners may have to pay these fines of out of the pocket and these regulatory fines and penalties um that followed companies actions whether they are negligent or intentional for non-compliance. As the GDPR S can be extensive, you know, business owners must plan accordingly with their uh finance, should they face these fines? And this is very typical again, because in your daily routine, you are using all your, you know, digital devices and you are using ecommerce and you always share your personal data with these companies, organizations. So this Cyber insurance is one of protector for GDPR, you know, penalties and the data breach issues too. And if you can continue in here, you can see it's not just for organizations, it's also cover the personal in cyber insurance issues too.

I mean that uh technology has become very extensive and so it's hard to live without it, you know, it comes with huge advantages but also risks. And there is an increasing role for insurance to play in protecting customers in the face of cyber threats besides being able to stop whenever or however, as well as stream movies and music, the di digital digitalization of the personal space and many many other more tangible benefits too for millions of people in emerging markets, men money via mobile phone has become a lifeline, rapid advance in um technology are inevitable new services all the time.

Smart doorbells, let you see who is at the doorstep via uh your app on your phone and smart heating, lighting controls. Let you change the temperature and the switch lights of remotely. All just all such these devices are part of internet um of things. I mean that IOT the meaning they are connected and send via internet and enabling them to be controlled by phone tablet or PC or Tle bots. Sky is the limit right now. There are many cyber text types that are targets individuals uh more specifically and which can have profound and distressing the consequences. And so you can face with this area, this identity protection, data, loose recoveries, cyberbullying connected from device attack protection, network extortion protection, mobile banking protection, because it can cause financial fraud. Most probably a lot of people face this kind of issues because every day we receive some message, some emails from different organizations from different financial area. And we have to face we have to understand these risks and we have to control these areas and the online transition and cyber liability.

And there are also cyber uh insurance solutions for people needs as the same as companies that is why that we can protect themselves from the cyber risks. And then finally, sorry. Yeah, we have some challenge in the sector, this negative and uh dynamics in cyber insurance markets.

But I believe that with all these negative issues can be solved and several lo long standing barriers and uptake, uh we can understand after that the potential for cyber insurance to, you know, incentivize negative behaviors like the moral hazard and ransom there. And all in all cyber insurance can be still considered very new and important. So uh Cyber insurance, I I think this insurance area can't be understood yet very well and technology is touching every aspects are lives and therefore it's very inevitable cycle. Insurance will become more and more critical. And uh my my perspective, I it is highly likely what we will start seeing the cyber insurance concepts in the form of cloud competing insurance, IOT insurance A I insurance or Blockchain insurance in the future. And although a well functioning cyber insurance industry could improve cybersecurity practices on a societal scale and it's very, very related with our cyber risks to control everything in our daily life. And I am very sure that the wonderful ladies like you will start taking place and add value in the field of cyber insurance, which is one of the emerging concepts and brings together, you know, cyber security risk management and financial sector approaches and wishing you good health and happiness.

And thank you for everyone, your time and listening and hope you will enjoy the conference. It's very nice to meet you all. Bye bye.